by Larry Levin

Another great article penned by analyst David Rosenberg of Gluskin-Sheff:

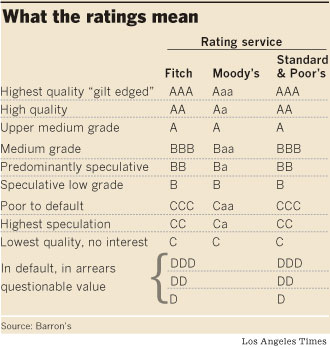

The drama continues following S&P’s slice to Greece’s debt rating (to junk status of BB+, a three-notch decline, which prompted a surge in 2-year bond yields to a Zeus-like 15%) and the two-notch decline to Portugal’s rating, to A- from A+. The Euro has bounced back this morning and the flight to higher quality German and French bonds has partly reversed course as the markets are swirling with speculation that the IMF is about to announce a stepped-up aid package (yet again!) and the ECB’s Trichet (“Mr. Euro” himself) is set to make a trip to Berlin to meet with German parliamentarians today. (In the U.S., the huge rally in Treasuries has subsided too as the bond market braces for $42 billion of fresh 5-year T-notes today). JGBs have rallied all the way to four-month lows, in terms of yield, to 1.28% — talk about a switch to defense (not to mention a slap in the face to the conventional wisdom that JGBs are an accident waiting to happen — see Clock is Ticking on Japan’s Low Debt Yields on page 23 of the FT).

The problem of course is that if Greece is bailed out then surely Portugal, Ireland, Spain and perhaps even Italy may not be too far behind. The inability of Greece — and others within EMU — to enact an independent monetary policy at a time of crisis has exposed the flaws of the union. The lack of a cohesive national government is another flaw in times of turbulence, which is why the U.S.A. has longevity and the Eurozone likely does not. It may well be the time to assess why it was that past attempts at unionization in the region — the Latin Monetary Union and the Scandinavian Monetary Union in the late 19th century — ultimately fizzled out.

While the Euro has come back this morning (temporary) from its year-low abyss, global equities are still reeling from the contagion concerns (the MSCI Asia Pac index down 1.5% today) and a stock market priced for perfection is once again confronting a world with blemishes. (Add to that the U.S. government’s attacks on Goldman Sachs as another blemish, at least as far as the investment community is concerned — even John McCain got involved in yesterday’s populist lynching: “From the reading of these emails, there is no doubt their behavior was unethical and the American people will render a judgment.”)

Anyone notice the volume on the U.S. exchanges swell as the selling picked up steam yesterday in yet another in the long list of “distribution” sessions? (Volume on the exchanges surged to a combined 7.6 billion shares — the second highest level for the year.) Portugal’s stock market has traded down to a 12-month low and it’s so bad in Greece that the government has banned short selling for two months. (Hey, it worked in the once-capitalistic U.S.A. didn’t it?) We see in the NYT that Barclay’s analysts believe that Greece needs €90 billion to see them through, €40 billion for Portugal and €350 billion for Spain!

That is €480 billion of refinancing help, which dwarfs the latest €45 billion EU-IMF joint aid announcement by a factor of TEN (according to Ken Rogoff, the IMF is maxed out after €200 billion)! Do euros grow on trees as fast as Bernanke-bucks? Would the ECB, modeled after the Bundesbank, ever resort to the printing press for a fiscal bailout? Where exactly is this money going to come from? You can see why commodities are still under pressure as V-shaped recovery hopes are given a sober second thought. Even in countries like Canada, small and open as it is, has seen its currency lose some of its altitude despite the widespread perception that the local economic and financial backdrop is pristine as can be (Canada is in relatively good shape, indeed, but we challenge some of that conventional wisdom below). What a time for the Bank of Canada to have moved the domestic money market to price in a 275 basis point tightening cycle. (Remember how the Asian crisis, which started with tiny Thailand, stopped the Fed’s planned rate hikes in 1997 in its tracks and who knew that time that more rate cuts were coming down the pike? How many times has the front end of the Canada curve looked this attractive before?)

With that in mind, the Fed had better be very careful about changing any of its wordings in today’s post-meeting press release (especially the day after the VIX index soars 30%). Recall the Bank of Canada’s strident tone last week (watered down a tad by Governor Carney in yesterday’s statement to the House of Commons) which prompted the money market or immediately price-in a rate hike at the June 1 meeting.

Yesterday was really as much, if not more, about Portugal than it was about Greece. Contagion risks are spreading as they were amidst the turmoil around Bear Stearns in early 2008 and we know how that turned out. Bear was not too big to fail; neither was Lehman thought to be at the time. And then the Obama team decided to bail out the other large banks with fiscal costs in the future that will massively constrain domestic economic growth.

Let’s look ahead — beyond Greece and Portugal to Spain. Its combined fiscal and current deficits are the highest in the industrialized world, save for Iceland (and we know what shape it is in). The amount of debt it has to refinance in the coming year is as large as the entire Greek economy (though the latter is getting smaller by the day). So this is not even a case of being too big to fail as much as being too interconnected globally to default. Think of all the global banks, most of them in Europe, which hold onto all this spurious Club Med debt. Moreover, if the other two major rating agencies follow S&P’s lead and cuts Greece to “junk”, then the ECB would be in a real bind for it cannot hold below-investment-grade bonds on its balance sheet. If the ECB does accept junk-rated

Greek debt as collateral, then the sanctity of its balance sheet will be seriously undermined; though this ostensibly didn’t matter too much to the Fed in the name of saving the system.

At the same time, refusing to accept Greek debt would exert tremendous strains on the European banking system (see Hobson’s Choice for Germany ECB on page C16 of the WSJ; and also have a look at Debt Crisis Poses Risks to ECB Balance Sheet on page A12 of the WSJ). Whether or not all these countries can be saved by the IMF, Germany or the ECB, the reality is that the downside to the Euro, even at 1.32, is huge. Think of a retest to the lifetime lows of 0.85 at some point down the line.

The Chinese stock market is down now for the fifth session in a row — the longest losing streak in 16 months and the lowest close since October 12, 2009 (dare we say when the S&P 500 was trading 100 points south of where it is today, and the Dow lower by a 1,000 points). And the index leads commodities by four months, so this is not exactly a constructive signpost as far as the near-term outlook for resource prices is concerned (see more below).

So, we have the problems in Euroland, signs of a property bubble in China, and the darling Brazilian economy now in overheating phase to such an extent that the central bank is about to hike rates 100bps in one fell swoop (did we mention the Henry Tax Review in Australia, which is due out on Sunday and set to propose tax changes for the resource and banking sectors?) — and yet all we hear from the rose-coloured bullish pundits is how we have to now measure the U.S. equity market based on “global considerations”, not merely the American economy. Yesterday, we heard a classic rear-view-mirror comment from UPS CEO Scott Davis that went: “Economies around the world are showing signs of recovery.” Every word in that comment was accurate except the tense — replace “are” with “were” (not to mention that this is classic top-of-the-market that defines the term “famous last words”).

Previous Day's Trading Room Results:

Trade Date: 4/29/10

E-Mini S&P Trades*

(before fees and commissions):

1) No "Secrets" trades were filled.

2) Algorithm positions (9)

3) “Reading the Tape” positions (7) …combined Secret’s, Algo, & “Reading the Tape” total…+7.50

Sign up as an AvidTrader Member to receive "The Technician" Value Area's each day. The market then has an 80% chance of filling the Value Area. Many traders familiar with the Value Area and the techniques that go along with it use it to help them decide what trades to do each day. Join and see how this technique can help you trade more successfully!

No comments:

Post a Comment